Complex dynamics shape the global automotive industry’s transition towards battery electric vehicles (BEVs). Today, Western automakers face strategic considerations and challenges amid evolving regulatory landscapes, geopolitical tensions, and competitive pressures, particularly considering China’s growing dominance in the BEV sector.

Recent media reports have suggested that the White House has been contemplating responding to political and industry feedback by potentially delaying the stringent EPA fuel economy regulations initially set for 2027-2032. This deliberation highlights the acute pressure original equipment manufacturers (OEMs) face in meeting near-term objectives, particularly those for 2026, deemed pivotal in the transition towards battery electric vehicles (BEVs).

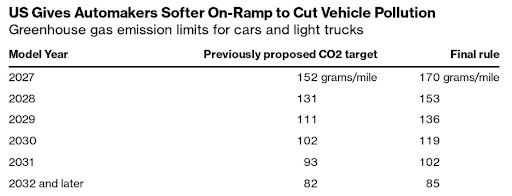

As of March 29, this speculation was put to bed when the EPA published its final rule on light, medium and heavy-duty vehicles. Its slightly revised trajectory still sets a daunting challenge for OEMs, which are estimated to require approximately a 9% pure BEV fleet by 2026, a steep climb from the roughly 3% achieved by the Detroit Big Three (D3) in 2023.

The shift from an original target of 152 grams of CO2 per mile (equivalent to 58 mpg) to the revised target of 170 grams per mile (52 mpg) in 2027 represents an easing of emissions standards. Similarly, for 2032, the adjustment from 82 grams of CO2 per mile (108 mpg) to 85 grams (105 mpg) also indicates a relaxation of the targets.

These changes suggest a minor recalibration rather than a wholesale reversal of the legislation’s strategic intent. For OEMs, the aggressive timeline for adopting new technologies and adjusting production plans remains the same. The final rule does not afford OEMs more breathing room to manage the transition, nor does it necessarily signal a shift away from the long-term goal of reducing emissions. These are still aggressive targets when you consider that by 2027, OEMs must achieve a fleet average of 52 mpg per vehicle, and five years later, that objective doubles to an OEM fleet average of 105 mpg per vehicle.

America’s Costly BEV Transition

Ambition, strategic complexities, and significant financial challenges mark the United States’ journey toward a BEV future. At the heart of this transition is President Joe Biden’s vision to foster a domestically centered BEV supply chain, as propelled by the Inflation Reduction Act (IRA). This initiative aims to bolster U.S. manufacturing prowess and reduce dependency on foreign components, particularly those sourced from China. Under Elon Musk’s stewardship, Tesla has emerged as a pillar of this American dream, making notable strides in localizing its supply chain with initiatives like sourcing batteries from Nevada and establishing a lithium refinery in Texas.

Despite these advances, Tesla’s recent engagement in procuring a record number of Chinese-made lithium-ion batteries have spotlighted the industry’s nuanced hurdles. This maneuver reflects a broader narrative of China’s dominance in the critical metals and minerals essential for battery production, contrasting starkly with the IRA’s intent to diminish Chinese influence in America’s BEV supply chain.

The comparison to China’s influence over battery materials being greater than OPECs over oil underscores the strategic importance of diversifying supply chains. The BEV transition in the U.S. is not merely an industrial shift but a geopolitical maneuver aiming to reduce dependency on a single, dominant player in the global market. This transition, marked by ambition and uncertainty, underscores the need for a concerted effort to build a resilient, diversified supply chain that supports the growth of a domestic BEV market without compromising economic and strategic autonomy.

The U.S. also faces a considerable challenge in expanding its BEV charging infrastructure. Despite the ambitious targets for BEV adoption and the push towards a green automotive future, the current state of charging infrastructure lags the needs of potential BEV consumers. The disparity between the number of BEVs on the road and the available charging stations creates a bottleneck, deterring consumers who are concerned about the convenience and feasibility of charging their vehicles.

The federal government, under initiatives like the Infrastructure Investment and Jobs Act, has allocated funds to expand the national charging network. However, the deployment of these funds and the actual construction of charging stations need to be accelerated to meet the growing demand for BEVs. Moreover, the focus should not only be on increasing the quantity of charging stations but also on their strategic placement, ensuring accessibility in urban as well as rural areas, and improving the charging speed to accommodate the needs of various users.

The slight adjustments to EPA’s 2032 emissions targets underscore the complex interplay of political dynamics, technological feasibility, and market readiness in the U.S. automotive sector. Political shifts, such as a potential Republican victory in upcoming elections, could recalibrate the current BEV-centric agenda, given the party’s historical preference for deregulation. This political backdrop is compounded by the auto industry’s skepticism regarding the attainability of future emissions targets amidst constraints in raw material availability and the prevailing technological landscape.

Moreover, as forecasted by S&P, the industry’s consensus anticipates a more conservative 50% BEV market share by 2030, diverging from more optimistic projections. This tempered expectation reflects a cautious outlook on the pace of BEV adoption and the challenges of transitioning from internal combustion engine (ICE) vehicles.

As America navigates this costly transition, the automotive industry grapples with balancing regulatory compliance, technological innovation and market dynamics. The stringent guidelines introduced by the Treasury in December to curtail reliance on Chinese components underscore the daunting task ahead for U.S. carmakers. Companies like GM and Ford, already facing financial strains in their BEV ventures, stand at a critical juncture, highlighting the imperative to develop a diversified, resilient supply chain that supports the domestic BEV market’s growth without sacrificing economic and strategic independence.

Europe’s BEV Crossroads

As Europe’s automotive industry navigates the pivotal shift towards BEVs, significant players like Volkswagen, Renault, and Stellantis are contemplating unprecedented collaborations to remain competitive. Faced with the dual challenges of emerging Chinese competitors and Tesla’s market dominance, these companies recognize the urgency to adapt or risk significant setbacks. Carlos Tavares, CEO of Stellantis, has voiced concerns over the European auto industry’s vulnerability, predicting a “bloodbath” if it fails to counteract Chinese competition effectively.

The backdrop to this evolving landscape is a notable slowdown in BEV adoption, compounded by reduced government incentives, increased repair costs, and consumer pushback against climate policies. This scenario is unfolding as stricter emissions regulations take effect in 2025, threatening manufacturers with hefty fines if they fail to meet the required quotas for battery-powered vehicles. Amidst this, Chinese manufacturers, backed by state support, are poised to enter the European market with cheaper and potentially superior models, exemplified by BYD’s Dolphin, priced at about €7,000 less than a similarly equipped VW ID.3.

In response, European carmakers are exploring various strategies to mitigate these challenges. Renault CEO Luca de Meo has proposed an “Airbus of autos” approach, suggesting a collaborative effort akin to the aerospace consortium to share the burdensome costs of developing affordable BEVs. This idea draws inspiration from Japan’s kei cars, which enjoy benefits from regulatory preferences due to a unified approach by manufacturers. Meanwhile, Stellantis’s Tavares is open to mergers and acquisitions, and Volkswagen has focused on internal cost-cutting measures, including workforce adjustments and production shifts.

Europe, while ahead of the U.S. in terms of charging infrastructure, still faces its own set of challenges. The European Union has set ambitious targets for the rollout of charging points across member states, aiming to address the increasing demand as BEV adoption rates rise. However, the uneven distribution of charging infrastructure across different countries and regions within Europe poses a significant barrier to the universal adoption of BEVs. Urban areas tend to have better infrastructure compared to rural regions, creating disparities in BEV feasibility for potential users.

The European Commission’s push for a significant increase in the number of charging points by 2025 is a step in the right direction. However, this initiative requires coordinated efforts from national governments, local authorities, and private sector stakeholders to ensure that the infrastructure development keeps pace with the growing BEV market.

The urgency for collaborative and innovative strategies is further underscored by the broader economic implications, with the automotive industry playing a critical role in the EU’s economy and employment. As European carmakers grapple with these transitions, the need for agility, innovation, and strategic partnerships has never been more apparent. This period of disruption and adaptation could very well define the future landscape of the global automotive industry, with European manufacturers striving to maintain their competitiveness in the face of a rapidly changing market.

The Strategic Considerations

The slightly slower path to EPA standards in the United States and similar European legislative measures designed to accelerate the automotive industry’s shift towards BEVs embodies a double-edged sword for Western automakers and economies. In the short term, delays present an earnings reprieve, granting Western OEMs and their suppliers a crucial window to capitalize on ICE vehicles. A Republican victory could allow these entities to bolster their financial reserves, refine BEV technologies, and strategically plan for a gradual transition. However, these short-term boon masks underlying long-term geopolitical and economic risks that could undermine the competitive stance of the U.S. and European automotive sectors in the face of China’s aggressive BEV push.

China’s central government has adeptly marshaled resources, policy, and industry to forge a dominant position in the BEV market, achieving unprecedented scale and setting the pace for global BEV adoption. This state-backed strategy enhances China’s automotive market share and secures its influence over the critical supply chain for BEV components, such as batteries and rare earth materials. The juxtaposition of China’s proactive stance against the West’s delayed regulatory action reveals a strategic gap that could have profound implications for Western economies and their automotive industries.

From a macroeconomic perspective, the automotive industry is a cornerstone of Western economies, contributing significantly to GDP, employment, and technological innovation. A delayed transition to BEVs risks ceding market leadership to China, impacting the automotive sector and the broader economy. As China consolidates its position in the BEV market, it could reshape global trade patterns, influence international standards, and dictate terms in critical technology and environmental policy areas. This shift could erode the industrial base of Western economies, leading to job losses, diminished R&D capabilities, and a dependency on China for essential technologies and materials.

For Western OEMs, the strategic risk lies in losing ground to Chinese competitors rapidly advancing in BEV technology, manufacturing scale, and market penetration. The longer Western OEMs rely on ICE vehicle sales, the more they risk lagging in the BEV race, potentially becoming niche players in a market they once dominated. This scenario would impact not only their market share and profitability but also their brand perception and relevance in a future dominated by clean energy vehicles.

The automotive supplier base, essential for innovation and production efficiency, faces substantial challenges. As the demand for ICE vehicle components diminishes, suppliers must shift focus towards BEV technologies. However, this shift has its financial and operational hurdles. Due to intense competition and insufficient scale, only a few suppliers are profitable in making BEV components and systems like E-Drives and batteries. The pressure to quickly profitable returns exacerbates the difficulty of this transition, potentially leading to mergers, bankruptcies, and a decline in technological leadership. Furthermore, as China tightens its control over the BEV supply chain, there’s a risk that Western suppliers may be relegated to a secondary role, increasingly reliant on Chinese materials and components.

To mitigate these risks, the United States, the European Union, and their associated industries must adopt a more aggressive and coordinated approach to BEV adoption and innovation. This includes investing in R&D, securing supply chains for critical materials, incentivizing BEV purchases, and fostering collaborations between OEMs, suppliers, and technology firms. Furthermore, engaging in diplomatic and trade strategies to ensure fair market access and competition is vital.

In conclusion, while a slight delay in EPA standards and European legislation offers a reprieve for automakers, it presents a strategic problem that could have far-reaching consequences for their long-term competitive positioning, the automotive supply chain, and the broader economy. Navigating this transition with strategic foresight, adaptability, and collaborative efforts is imperative for these economies to maintain their automotive leadership and secure their economic futures in the face of China’s rising BEV dominance.

Software Do?")