Last mile costs rising fast

Last mile costs rising fast

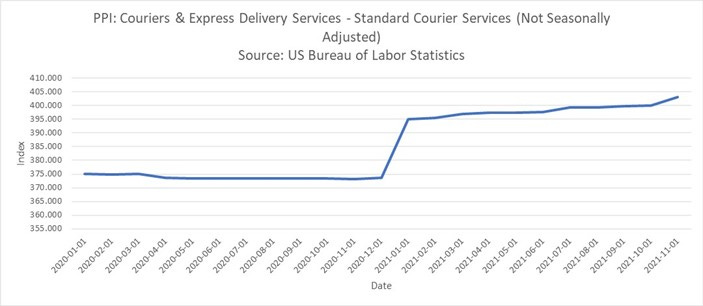

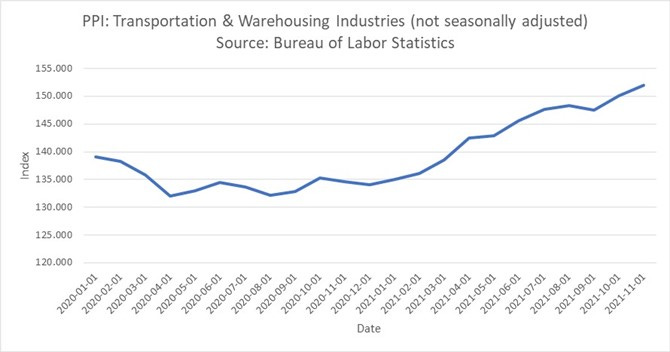

Year-over-year PPI for standard courier services increase faster than overall transportation & warehousing

Last-mile costs are outpacing overall transportation and warehousing costs, a trend likely to continue through 2022.

According to the US Bureau of Labor Statistics’ producer price index (PPI) for couriers and express delivery services, standard courier services have increased 30.023 points from November 2020 to November 2021, index based on 1992=100 and not seasonally adjusted. In comparison, transportation and warehousing PPI increased 17.844 points for the same period, index based on 2006=100 and not seasonally adjusted.

Note in the first chart, Standard Courier Services PPI Index, the sharp jump from December 2020, 373, to January 2021, 394.

The 2020 holiday season was one of delivery delays and insufficient capacity for many last-mile carriers as more consumers shopped online versus in-stores. This combination resulted in higher shipping costs for retailers. Higher shipping costs carried over into January 2021 as remaining delayed holiday parcels were delivered, holiday returns were processed, and annual rate increases, including higher surcharges from last-mile carriers, took effect.

Despite increasing rates and surcharges, last-mile carriers’ costs continue to grow as strong consumer spending and the recovery of business-to-business (B2B) spending continue.

Year-to-date through November, retail sales are up 18.3% year-over-year, while e-commerce retail sales are up 12.1% year-over-year through the third quarter, according to the US Census Bureau.

During FedEx’s fiscal second quarter for the period ending November 30, the company noted that its Ground Commercial (B2B) delivery service reported an 8.7% year-over-year increase in terms of average daily volumes. However, as noted by FedEx executives, B2C volumes remain higher than pre-pandemic levels.

The increased demand and rising oil prices prompted FedEx and UPS to increase their fuel surcharges at least twice during 2021 and UPS to their fuel surcharge once more, effective today, January 3, after a previous adjustment in November.

In addition, FedEx, in particular, has not been immuned by the “Great Resignation.”

“The difficult labor market once again had the largest effect on our bottom line, representing an estimated $470 million in additional year-over-year costs,” FedEx CFO Mike Lenz told analysts on December 16. “Of the $470 million, we estimate $230 million was incurred in higher wage and purchase transportation rates. This included higher wage rates and paid premiums for team members and higher rates paid for third-party transportation services. We estimate network inefficiencies resulting from labor shortages, increased costs by approximately $240 million. These costs include additional line-haul, higher usage of third-party transportation, cost to reposition assets in the network over time, and recruiting incentives all to address staffing shortages,” Lenz said.

2022 and beyond

As we begin 2022, higher last-mile rates and surcharges go into effect for carriers. Retailers will likely encourage curbside pickups and Buy Online, Pickup in Store (BOPIS) options to mitigate costs.

Other retailers, such as AEO, will acquire middle and last-mile capabilities to manage last-mile costs. In contrast, other retailers, such as Walmart, will offer their own last-mile services.

In addition, expect more technology investments and more startups to enter the last-mile market this year as retailers continue to invest in omnichannel strategies and offer faster delivery services.

The last mile will be under intense scrutiny this year as retailers look to reduce costs while managing even more deliveries.

By 2026, the US domestic parcel market is expected to reach 134 million pieces, a 70% increase from 2020, according to FedEx. E-commerce is expected to drive 90% of the parcel market growth. Meanwhile, the US domestic B2B market will grow at a 5% CAGR through 2026.

For more, check out a couple of previous articles:

Help Wanted - Delivery Drivers

- Cathy

That’s about it for now. Thanks for reading. While I aim for a weekly story, sometimes life gets in the way, so think about subscribing (free) so that you don’t miss anything.

For daily thoughts and shares, be sure to follow me on Twitter and LinkedIn.

I wear a number of hats these days. Besides running a logistics market research firm, catch my weekly articles on air cargo, freight forwarding, and the express markets, as well as a monthly podcast on Air Cargo World, I’m also trying to figure out how to measure returns for the Reverse Logistics Association, I assist companies with content and other needs and I’m trying to figure out how to update my website (which is down at the moment).