Weekly highlights

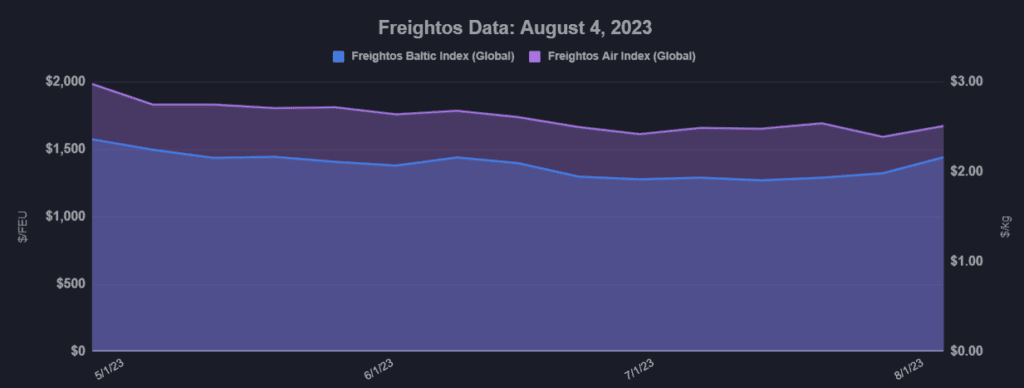

Ocean rates – Freightos Baltic Index:

- Asia-US West Coast prices (FBX01 Weekly) increased 9% to $1,672/FEU.

- Asia-US East Coast prices (FBX03 Weekly) increased 3% to $2,667/FEU.

- Asia-N. Europe prices (FBX11 Weekly) climbed 31% to $1,655/FEU.

- Asia-Mediterranean prices (FBX13 Weekly) increased 18% to $2,345/FEU.

Air rates – Freightos Air index

- China – N. America weekly prices decreased 12% to $3.48/kg

- China – N. Europe weekly prices increased 2% to $3.14/kg.

- N. Europe – N. America weekly prices fell 6% to $1.69/kg.

Dive deeper into freight data that matters

Stay in the know in the now with instant freight data reporting

Analysis

August General Rate Increases (GRI) pushed ex-Asia ocean rates up sharply to start the month on a combination of demand rebounds and stricter capacity reductions by carriers.

Transpacific weekly average rates increased to $1,672/FEU to the West Coast last week, and $2,677/FEU to the East Coast. But West Coast prices have climbed to $1,900/FEU so far this week, a 44% increase compared to mid-July and 23% higher than in 2019. East Coast rates reached $2,883/FEU yesterday, a 20% increase since mid-July and 2% higher than in 2019.

These price increases are partly driven by some demand recovery.

National Retail Federation US ocean import data estimates that July volumes increased 4% compared to June. And though July numbers would be 3% lower than in 2019, imports are projected to increase in August and remain elevated through October – in line with typical seasonality and 3-6% above 2019 levels. Based on projections through December, total 2023 volumes would show 3% growth relative to 2019, slightly below the 2012 – 2019 average annual growth rate of 4.2%.

But even as peak season gets underway, carriers are having to reduce capacity in order to get rates to climb, reflecting the generally over-supplied state of the market as fleet sizes continue to grow.

Another factor for Asia – US East Coast rates is the low water level in the Panama Canal. Though some surcharges and restrictions have been in place since June without significant impacts on rates or operations, the first reports of congestion and a ship having to offload containers before entering the canal this week point to the potential for this situation to cause disruptions.

Asia – Europe GRIs pushed ocean rates to $1,655/FEU last week and up to $1,782/FEU so far this week, a 37% increase on July and 28% higher than in 2019. This lane has seen moderate volume growth in the last few months with June imports 3% higher than last year. But like on the transpacific, the rate climb is only likely to stick if accompanied by significant and sustained capacity reductions.

Asia – Mediterranean demand remains particularly strong, and has been the driver of rates remaining above 2019 levels this year even as prices fell on other trade lanes. As carriers added capacity to the lane prices fell about 17% in July from the elevated level of about $2,400/FEU it had sustained since April, but a GRI last week has pushed prices back up to $2,423/FEU this week, 38% higher than in 2019.

Transatlantic volumes meanwhile have been declining gradually since last May, and in June dipped below 2019 levels. Carriers had shifted capacity to this lane earlier in the year as transpacific demand sagged, but as volumes and rates – this week at $1,688/FEU – fall below pre-pandemic levels, carriers are beginning to shift capacity away.

In labor news, the ILWU Canada membership ratified the revised agreement with port operators late last week, putting an end to the dispute that had shut down Canadian ports for the first half of July. US LTL carrier Yellow, which had ceased operations last week and blames Teamsters for hastening its demise, filed for bankruptcy protection this week, with competitor XPO announcing a planned increase in capacity as Yellow has exited the market. In air cargo, some observers think the demand lull has reached its floor and should start a gradual recovery. For now Freightos Air Index data shows Asia – Europe air rates have been stable, at about the $3/kg level since about May with weekly rates ticking up 2% to $3.14/kg last week, about 40% lower than a year ago. Transpacific rates fell 12% this week to $3.48/kg, more than 50% below last year and transatlantic prices fell 6% to $1.69/kg and 44% lower than last August.

Freight news travels faster than cargo

Get industry-leading insights in your inbox.