Weekly highlights

Ocean rates – Freightos Baltic Index

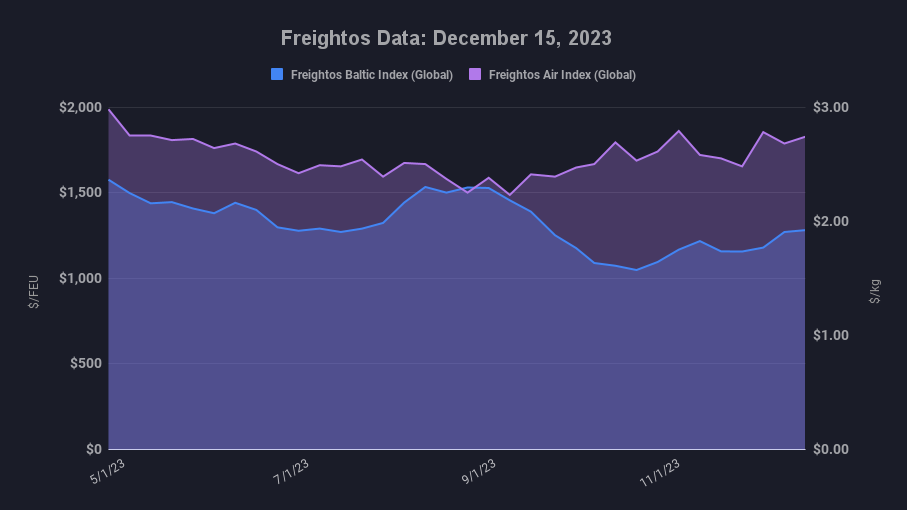

- Asia-US West Coast prices (FBX01 Weekly) fell 3% to $1,556/FEU.

- Asia-US East Coast prices (FBX03 Weekly) were level at $2,509/FEU.

- Asia-N. Europe prices (FBX11 Weekly) were also level at $1,467/FEU.

- Asia-Mediterranean prices (FBX13 Weekly) increased 12% to $2,414/FEU.

Air rates – Freightos Air Index

- China – N. America weekly prices were level at $5.86/kg

- China – N. Europe weekly prices increased 30% to $4.78/kg.

- N. Europe – N. America weekly prices increased 3% to $2.22/kg.

Dive deeper into freight data that matters

Stay in the know in the now with instant freight data reporting

Analysis

An increase in Houthi missile and drone attacks on ships – including container vessels operated by Maersk, MSC and others – last week led four of the top five largest container carriers to announce they will be avoiding the Red Sea and the Suez Canal until security is restored to the waterway. Together with ZIM who was already diverting their Red Sea traffic, these carriers represent 56% of global capacity, meaning an estimated 17% of global volumes will be taking a longer, more expensive route from Asia around the southern coast of Africa to N.Europe and the Mediterranean, as well as some Asia – N. America traffic.

In response, the US Department of Defense announced the launch of Operation Prosperity Guardian which will work alongside existing navy assets in the region to address the Houthi threat and will include support from the United Kingdom, Bahrain, Canada, France, Italy, Netherlands, Norway, Seychelles and Spain.

Container diversions will take an extra 7-14 days in transit time depending on the lane, and mean a 15-20% increase in costs for carriers. In addition to longer voyages and higher costs, disruptions to scheduled arrival times could cause congestion at destination ports and some equipment shortages as empty containers take longer to get back to origin ports.

Asia – N. Europe and Mediterranean ocean prices had been climbing on December GRIs even before the announced diversions, with rates to Europe up 21% $1,467/FEU and to the Mediterranean up 62% to $2,414/FEU since the end of November. Rates so far this week have continued increasing to about $1,560/FEU to Europe and $2,600/FEU to Mediterranean destinations.

But those rate increases were likely only achieved on the back of significant blanked sailings by carriers trying to bring high capacity levels – driven by growing fleet sizes – to the level of demand. Some carriers were already extending service suspensions into 2024 as supply and demand are misaligned. Now, carriers will devote those extra vessels to services traveling longer distances and requiring more ships to keep to existing departure schedules.

Asia – N. Europe and Mediterranean ocean rates will almost certainly increase due to the higher costs needed for these diversions. ZIM, which was already diverting its vessels that normally use the Red Sea, increased rates for its Asia – Mediterranean service, up to the $3,300-$3,400/FEU range last week. But because of the excess capacity available to address the disruption – something that was not the case during the Suez Canal blockage in 2021 – it is possible that the industry will avoid the extreme rate spikes like those seen during the pandemic.

So, shippers on affected lanes should expect longer lead times and higher freight rates until the Houthi threat is brought under control. But operations could continue reasonably well until then, and freight rates are unlikely to spike to extreme highs due to the current high levels of available capacity. With the international community mobilizing and motivated to remove this disruption to global trade, it is also possible that these diversions will not last very long.

You can access our full report on the Red Sea disruption impact here.

On the transpacific, ocean rates were stable overall last week. Looking toward 2024, reports of robust holiday sales in November in the US points to the continued strength of US consumers, and suggests that importers will enter a restocking cycle after the holidays. And, just as daily transits through the Panama Canal were set to drop from 22 to 20, authorities announced transits will instead increase to 24 a day in January due to new conservation measures and water level developments.

China – N. Europe air cargo rates, which had been declining since the end of November, rebounded last week to more than $4.50/kg back to about its November level. This increase could indicate some shippers are shifting some time-sensitive shipments from ocean to air as ocean shipments will now take longer to arrive due to widespread diversions.

Freight news travels faster than cargo

Get industry-leading insights in your inbox.