This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In today’s architectures and functional metrics, value optimization does not exist. And, when procurement and tactical planning operate in isolation, there is no decision support framework to guide the trade-offs especially when the functions are tethered to different and conflicting metrics. You are right.

The use of orbit charts allowed me to see the patterns of performance at the intersection of metrics over time. The second part of the story is that inventory turns for Lenovo are 10.8, Ranking at #13, PepsiCo outperforms on inventory turns, but performance is declining. For the past decade, I have been studying these patterns.

We talk about the move from functional metrics to a balanced scorecard, but we don’t use a balanced scorecard as an objective function. Orbit charts of four companies for the period of 2013-2022 at the intersection of operating margin and inventory turns. We speak of data latency, but do not measure the impact on performance.

Instead, what I observed when I looked at the data, was that most companies that I had worked with (in my role as an industry analyst, I had worked with over 300) were going backwards on margin and inventory turns. Resiliency is the pattern at the intersection of operating margin and inventory turns. “Ugh,” I said.

An average margin of 21% with inventory turns of 1.58 Sanofi Performance Versus Peer Group for 2013-2022 Similarly, I find 35% of companies following the pack not able to drive resilience in the face of market shifts. The performance in 2022 is almost the same as that in 2013 (note the circular pattern). Challenge this paradigm.)

The companies were selected based on performance better than peer group for 2006-2013 and delivering better than average improvement within the peer group as determined by the Supply Chain Index. However, due to a variety of factors, companies are losing ground on driving progress on both inventory turns and operating margin.

While the performance rankings were based on comparisons of inventory turns, operating margin and Return on Invested Capital (ROIC) for the periods of 2006-2013 and 2009-2013, the concept is that to be a supply chain leader you must outperform and drive improvement. Aligned Metrics. Supply Chain Design.

turns in 2013. Kellogg posted 19% margin in 2013 and 6.96 turns in 2013 but fell to 11% margin and 6.05 Orbit Charts for Kimberly-Clark and Kellogg for 2013-2022 A good friend of mine, asked, “Isn’t this the impact of the pandemic.” This work completed in 2013 defined the Supply Chains to Admire.

But the sheer complexity of supply chain networks, and the impact design decisions have on operational performance, makes supply chain inventory management aligning inventory investments with on-time customer delivery and margins a major challenge. trillion in cash according to a 2013 US Working Capital Survey.

SAP Announces Second Quarter and First Half Results 2013. Here are some additional details from the press release: Data Services data sets will include mode-specific transportation costs and transit times, facilities cost estimates, demographics, risk metrics, duties and taxes, sustainability metrics and others.

The research tries to establish “ who did supply chain best ” by looking at a weighted formula of Year-over-Year Growth, Return on Assets (ROA), and Inventory Turns for the Fortune 500 companies. Inventory Turns values are based on an average of quarterly reporting for the past year. Inventory Turns is only part of the story.

The relationship between corporate financial performance and supply chain metrics was complex; and in my first attempts, I was unable to derive a correlation. I wanted to better understand which metrics truly mattered. However, as many of you know, I am stubborn. I wanted to know more. I hungered to know the patterns. Definitions.

The future inventory fire sale. One of my stark realizations this year is that smaller companies are beating larger and often more established companies on growth metrics, inventory turns, operating margin, and Return on Invested Capital (ROIC). (In The metrics selection resulted from work with Arizona State University in 2013.)

Chainalytics Creates New Metrics for Demand Planning Consortium. Tweet The post This Week in Logistics News (May 13-17, 2013) appeared first on Talking Logistics with Adrian Gonzalez. In other news… Descartes Signs SuiteCloud Developer Network Agreement With NetSuite. HighJump Software Announces New Partnership With NetSuite.

Early 2012 marked the end of the third decade and 2013 finds us into the fourth. It comes in many flavors–increase in inventory, changes in sales policies, new product lines– all add to the complexity. The only industry that has made progress in inventory management is consumer electronics.

3 Key Metrics for Measuring Supply Chain Performance Beyond Cost Reduction. Inventory measurement is critical and it is money after all in that it took a capital expense to procure. Inventory measurement is critical and it is money after all in that it took a capital expense to procure. Cost reduction is still very important.

It is a quest and the subject of my next book, Metrics That Matter , that will publish in September, 2014. We used the period of 2006 to 2012 to build the model and we used the formula to attempt to predict 2013. And, recently, Procter & Gamble is more focused on improving inventory turns. I shake my head. What did we learn?

I have taken myself off the road to write the book Metrics That Matter. On the 2nd of April, I sat before a board discussing how a company could exceed expectations in the delivery of Return on Invested Capital (ROIC) and superior operating margins and fail at the delivery of customer service and inventory. It is a slow week.

We have found that supply chain metrics are gnarly and complicated.During We believe that a supply chain leader is defined by both the level of performance on the Effective Frontier (balance of growth, Return on Invested Capital, Profitability and Inventory Turns) and driving supply chain improvement.

Today, 90% of publicly-traded companies are stuck at the intersection of operating margin and inventory turns. While most companies have been able to make progress in one of these two critical metrics in the period of 2006-2013, they have not been able to make progress on both together. It is needed.

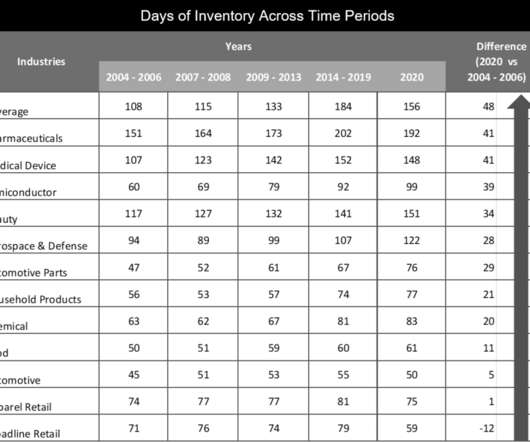

Companies tightly coupling the budget to S&OP have significantly higher inventories and lower growth than their peer group. Deployment of deeper statistical engines for inventory management with a focus on safety stock will improve inventory levels. Industries carried on average 32 days more inventory in 2020 than in 2007.

If the arrow is red, the industry is moving backwards on a metric. The industry made progress on revenue/employee, but struggled on growth, margin, inventory turns. We started the analysis to guide our own research and started sharing it with the industry in 2013. Companies, based on culture, tend to focus on singular metrics.

Companies with the lower score on the Index are driving faster rates of metrics improvement. Energizer and Unilever are driving the fastest rates of improvement and Clorox and P&G improvement rates are the slowest on the Metrics That Matter of Growth, Operating Margin, Inventory Turns, and Return on Invested Capital (ROIC)).

The companies were selected based on performance better than peer group for 2006-2013 and delivering better than average improvement within the peer group as determined by the Supply Chain Index. However, due to a variety of factors, companies are losing ground on driving progress on both inventory turns and operating margin.

Over the period of 2009-2015 only 88% of companies made improvement on the “Supply Chain Metrics That Matter.” (The The Supply Chain Metrics That Matter are a portfolio of metrics which correlate to higher market capitalization. Inventory Turns. We eliminate the lower 1/3 of companies for the period from consideration.

With the national warehouse vacancy rate hovering at record lows and warehouses bloated with inventory pulled in from China during 2018 to get ahead of impending tariffs, companies can combine flexible storage options with advanced technology to create an end-to-end supply chain solution that works. during the third quarter to $7.21

In our work on the Supply Chains to Admire report , we tracked the progress of manufacturing, retailing and distribution companies for the period of 2006 to 2013 and 2009-2013. We then rated companies on their ability to manage and improve a portfolio of metrics: operating margin, inventory turns and Return on Invested Capital (ROIC).

” Institute for Manufacturing, 2013. __. I think about this discussion with Keith often as I work on the Supply Chain Index and edit the chapters of Metrics That Matter. However, no company in this chart is on a linear path towards improving both margin and inventory turns. Tipping points are fascinating to watch.

I have a short list of retailers that I am watching that I think will fail in 2013 due to the lack of this understanding. Multiple channels are competing for inventory and this requires a new form of interoperability. Recently, I was facilitating a session at a Retail Connections conference on the “Role of the Store in 2013.”

Completed in 2012, the ERP project forced the company to standardize organizational design, roles, and metrics. They saw a steady drop in inventory and reduced working capital by about 50% over the period of 2011-2015. Impact of Demand Sensing on Inventory Levels. The reason? The implementation was very successful.

As we’ve seen over the past few years, businesses will keep automating and integrating supply chain planning capabilities, including demand-sensing, dynamic safety-stock management, inventory optimization, and external collaboration. In 2013, Target experienced a data breach that exposed the personal information of 40 million customers.

Inventory Turns (15%) (based on 2014 results). Growth 10% (Year-over-Year comparison of 2013 versus 2014). Supply chain leaders manage a complex system of non-linear, but very inter-connected metrics. Leaders need to balance a portfolio of metrics. Year-over-year Improvement at the Intersections of the Metrics.

For the past five years, the team at Supply Chain Insights identified Supply Chains to Admire Award Winners by analyzing performance by peer group on the key metrics of growth, operating margin, inventory turns and Return on Invested Capital (ROIC). In 2013, the company drove scale for finished goods. Meet Ernest.

McDonald’s has an inventory turn of 174.5. Microsoft acquired them in 2013, the company then laid off 12,500 people in 2014, then acquired Alcatel Lucent only to sell off a business unit to Foxconn. In this area, Gartner should push the metrics benchmark. Somehow, normalize the odd numbers. Nokia was tops at 46%.

For the past five years, the team at Supply Chain Insights identified Supply Chains to Admire Award Winners by analyzing performance by peer group on the key metrics of growth, operating margin, inventory turns and Return on Invested Capital (ROIC). In 2013, the company drove scale for finished goods. Meet Ernest.

The “Top 15 Supply Chains to Admire” is the culmination of a two-year effort to evaluate supply chain performance and improvement for the years of 2006-2013 by industry by vertical for publicly-held companies.

The success of the third-party logistics industry is evident in the generally high marks given to 3PLs by respondents to a survey as part of the 2013 17th Annual Third Party Logistics Study, which identifies trends and explores how both 3PLs and shippers are using these relationships to improve and enhance their businesses and supply chains.

Over the period of 2009-2015, only 88% of companies made improvement on the Supply Chain Metrics That Matter. To meet the criteria for The Supply Chains to Admire for 2016, companies needed to score better than their peer group average for performance metrics, while driving a higher level of improvement than 2/3 of their industry peer group.

In the process of compiling the Supply Chains to Admire report for last year’s Supply Chain Insights Global Summit , the research team at Supply Chain Insights calculated the rate of supply chain improvement of companies by industry for the period of 2006-2013 and 2009-2013. We studied this pre and post-recession.

Against this backdrop, it is interesting that many companies still depend on spreadsheets for demand planning and S&OP , as noted in the recent survey by APICS ( see Are Spreadsheets the Answer , SC Digest, September 2013 ). They had faster turns, lower inventory, and better customer service. I think so.

The two companies’ results on operating margin and inventory turns are shown in figure 1. Owens Illinois is investing 3X more in R&D than Sonoco Products; yet Sonoco products had 5X greater growth with 1/2 the inventory. Alignment on a Metrics Portfolio. Notice the more controlled pattern of Sonoco products.

The two companies’ results on operating margin and inventory turns are shown in figure 1. Owens Illinois is investing 3X more in R&D than Sonoco Products; yet Sonoco products had 5X greater growth with 1/2 the inventory. Alignment on a Metrics Portfolio. Notice the more controlled pattern of Sonoco products.

List of Top 10 Supply Chain Analytics Books 1) Supply Chain Metrics that Matter (Wiley Corporate F&A) 1st Edition This book offers an in-depth guide to understanding the link between corporate financials and supply chain maturity, evaluating the progress of over a hundred companies from 2006-2013.

And yet, prior to replacing a legacy inventory management system and implementing a supply chain analytics solution from FusionOps , the share of merchandise the company delivered on-time and in-full was a dismal 28 percent! How did this vast improvement in a key supply chain metric translate into financial performance?

We organize all of the trending information in your field so you don't have to. Join 102,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content