This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In comparison, in 2000-2007 the U.S. These schedule interrutions are "variability" that is disrupting flow and, thereby, increasing lead-times, using unplanned capacity and generating excessive (and still unbalanced) inventories. I think we could lose 10% of Capacity in many areas. That is huge progress to celebrate!

In comparison, in 2000-2007 the U.S. These schedule interrutions are "variability" that is disrupting flow and, thereby, increasing lead-times, using unplanned capacity and generating excessive (and still unbalanced) inventories. I think we could lose 10% of Capacity in many areas. That is huge progress to celebrate!

Freight volumes were mixed but mostly down, as the “freight recession” continued on now for more than two years. The Freight Tonnage Index from the ATA for June showed volumes in Q2 basically flat versus Q1, up just 0.2%. In comparison, in 2000-2007 the U.S. per gallon, and ending in June at $3.72, with a peak of $3.77

In comparison, in 2000-2007 the U.S. These schedule interrutions are "variability" that is disrupting flow and, thereby, increasing lead-times, using unplanned capacity and generating excessive (and still unbalanced) inventories. I think we could lose 10% of Capacity in many areas. That is huge progress to celebrate!

“Supply chain planners are often very skilled at mathematics and operational minutiae, but they typically haven’t mastered the storytelling skills required to make business cases for earlier, higher-quality engagement and for making strategic capacity investments to support future demand,” Aronow observes. In comparison, in 2000-2007 the U.S.

In comparison, in 2000-2007 the U.S. These schedule interrutions are "variability" that is disrupting flow and, thereby, increasing lead-times, using unplanned capacity and generating excessive (and still unbalanced) inventories. I think we could lose 10% of Capacity in many areas. That is huge progress to celebrate!

In comparison, in 2000-2007 the U.S. These schedule interrutions are "variability" that is disrupting flow and, thereby, increasing lead-times, using unplanned capacity and generating excessive (and still unbalanced) inventories. I think we could lose 10% of Capacity in many areas. That is huge progress to celebrate!

In comparison, in 2000-2007 the U.S. These schedule interrutions are "variability" that is disrupting flow and, thereby, increasing lead-times, using unplanned capacity and generating excessive (and still unbalanced) inventories. I think we could lose 10% of Capacity in many areas. That is huge progress to celebrate!

Click here to send us your comments In response, the National Motor Freight Traffic Association (NMFTA) has just released a framework it says can help shippers, carriers and brokers fight back against the growing and increasingly sophisticated threat of digitally enabled cargo theft. In comparison, in 2000-2007 the U.S.

First published in 2007, this classic reflection contrasts two distribution centers to show how mutual respect drives better results, stronger culture, and lower turnover. This article, originally published in 2007, offers insight into the value that problem-solving brings to corporate culture. In comparison, in 2000-2007 the U.S.

Click here to send us your comments That according to a recent blog post by the maritime analysts at Drewry, which noted that “More than five years have passed since the huge shipping disruptions, damaging port congestion, and cost spikes of the Covid period, but one feature has remained: freight rate volatility.”

Eurasian Rail Freight: Demand for rail freight between Asia and Europe has surged, leading to congestion and longer booking times. In comparison, in 2000-2007 the U.S. I think we could lose 10% of Capacity in many areas. Contingency planning for alternative ports is essential. That is huge progress to celebrate!

In comparison, in 2000-2007 the U.S. These schedule interrutions are "variability" that is disrupting flow and, thereby, increasing lead-times, using unplanned capacity and generating excessive (and still unbalanced) inventories. I think we could lose 10% of Capacity in many areas. That is huge progress to celebrate!

In comparison, in 2000-2007 the U.S. These schedule interrutions are "variability" that is disrupting flow and, thereby, increasing lead-times, using unplanned capacity and generating excessive (and still unbalanced) inventories. I think we could lose 10% of Capacity in many areas. That is huge progress to celebrate!

All that is distant memory now, as the maker of freight trucks powered by hydrogen fuel cells announced it had begun selling off its assets. In comparison, in 2000-2007 the U.S. I think we could lose 10% of Capacity in many areas. companies are reshoring and foreign companies are investing in U.S.

The monthly report from Cass and partner Tim Denoyer of ACT Research is based on data from the billions of dollars of freight bills that Cass pays for its shipper clients. in 2024, and so far is trending toward another decline in 2025, Cass says, as carriers navigate the lousy freight environment. In comparison, in 2000-2007 the U.S.

Meanwhile, our supply chain and logistics stock index, which is made up of more than 20 stocks across freight carriers, logistics service providers, and supply chain hardware and software vendors, lagged the S&P, with a gain of just 10.3% In comparison, in 2000-2007 the U.S. I think we could lose 10% of Capacity in many areas.

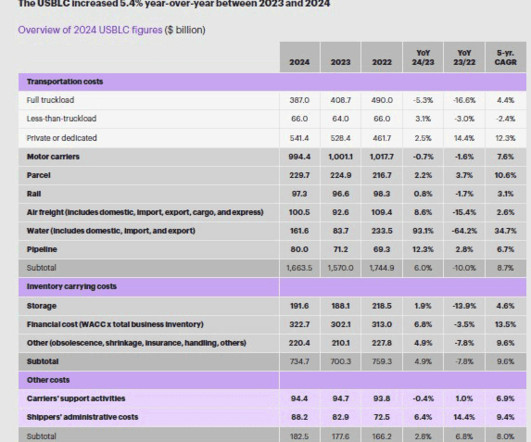

"Other" costs - always somewhat vague, and mostly involving certain IT expenses and some services such as freight forwarding, were up 2.8%, though this bucket is by far the smallest of the three main categories at just 7.0% In comparison, in 2000-2007 the U.S. The second component of USBLC, inventory carrying costs (28.4%

In comparison, in 2000-2007 the U.S. These schedule interrutions are "variability" that is disrupting flow and, thereby, increasing lead-times, using unplanned capacity and generating excessive (and still unbalanced) inventories. I think we could lose 10% of Capacity in many areas. That is huge progress to celebrate!

He founded a new freight company called “Federal Express,” to denote his national ambitions. In comparison, in 2000-2007 the U.S. These schedule interrutions are "variability" that is disrupting flow and, thereby, increasing lead-times, using unplanned capacity and generating excessive (and still unbalanced) inventories.

In comparison, in 2000-2007 the U.S. These schedule interrutions are "variability" that is disrupting flow and, thereby, increasing lead-times, using unplanned capacity and generating excessive (and still unbalanced) inventories. I think we could lose 10% of Capacity in many areas. That is huge progress to celebrate!

In comparison, in 2000-2007 the U.S. These schedule interrutions are "variability" that is disrupting flow and, thereby, increasing lead-times, using unplanned capacity and generating excessive (and still unbalanced) inventories. I think we could lose 10% of Capacity in many areas. That is huge progress to celebrate!

In comparison, in 2000-2007 the U.S. These schedule interrutions are "variability" that is disrupting flow and, thereby, increasing lead-times, using unplanned capacity and generating excessive (and still unbalanced) inventories. I think we could lose 10% of Capacity in many areas. That is huge progress to celebrate!

In comparison, in 2000-2007 the U.S. These schedule interrutions are "variability" that is disrupting flow and, thereby, increasing lead-times, using unplanned capacity and generating excessive (and still unbalanced) inventories. I think we could lose 10% of Capacity in many areas. That is huge progress to celebrate!

In comparison, in 2000-2007 the U.S. These schedule interrutions are "variability" that is disrupting flow and, thereby, increasing lead-times, using unplanned capacity and generating excessive (and still unbalanced) inventories. I think we could lose 10% of Capacity in many areas. That is huge progress to celebrate!

Replenishment of the split case locations became the bottleneck, in part because of an issue I still have never seen a great solution for: when volumes for a wave will wipe out a location’s inventory, but the required replenishment exceeds the location’s capacity when it arrives. In comparison, in 2000-2007 the U.S.

In comparison, in 2000-2007 the U.S. These schedule interrutions are "variability" that is disrupting flow and, thereby, increasing lead-times, using unplanned capacity and generating excessive (and still unbalanced) inventories. I think we could lose 10% of Capacity in many areas. That is huge progress to celebrate!

See More Below) CATEGORY SPONSOR: SOFTEON “The global forecast for new warehouse capacity in 2025 has been revised upward slightly, but still remains in negative territory at -2.0% In comparison, in 2000-2007 the U.S. I think we could lose 10% of Capacity in many areas. year-over-year out to 2030.

In comparison, in 2000-2007 the U.S. These schedule interrutions are "variability" that is disrupting flow and, thereby, increasing lead-times, using unplanned capacity and generating excessive (and still unbalanced) inventories. I think we could lose 10% of Capacity in many areas. That is huge progress to celebrate!

In comparison, in 2000-2007 the U.S. These schedule interrutions are "variability" that is disrupting flow and, thereby, increasing lead-times, using unplanned capacity and generating excessive (and still unbalanced) inventories. I think we could lose 10% of Capacity in many areas. That is huge progress to celebrate!

TuffAir’s site states that it plans to launch in the fall, “with high performance aircraft, lean operations and a scalable model to connect overlooked freight corridors across the Midwest. TuffAir argues that its strategy is unique and is designed to facilitate cheaper, faster regional air transit for freight. ( What do you say?

In addition, with no end in sight for ongoing freight market weakness, rolling stock that doesn’t have a traditional internal combustion engine is seen by many as too pricey for all but the deepest-pocketed carriers. In comparison, in 2000-2007 the U.S. kilowatt-hour (kWh) per mile. An y reaction to t hese stories?

And it’s about to get hit by a freight train of innovation. How much do we love freight innovation? Enough to go through every single article published in the top tech blogs – Techcrunch, Verge, Mashable and Recode – since 2007 to count how often articles about logistics startups, freight or cargo were published.

miles out of its network from 2007-2010 and had increased its CWT per truck from 382 in FY 2007 to 415 in FY 2010, an 8.6 Put differently, in FY 2007, Del Monte left 11.2 For related commentary, see Transportation Collaboration: Optimizing Freight Costs by Sharing Capacity and 5 Principles for Greener Freight.

The difference between BlackBerry in 2007— with a net worth of US $40B and BlackBerry in 2013—willing to be sold for a measly a tenth of its 2007 figure—has a lot to do with a failure to identify and deal with its competitors in the correct way. In 2007, it released the Kindle. Co-opetition can Save the Freight Industry.

It was made possible by a foundation of pricing and capacity automation dating back to Sabre’s reservation system in the ‘60s. JOIN OVER 1,000 TOP FORWARDERS AND CARRIERS AUTOMATING AIR FREIGHT. DISCOVER AIR FREIGHT SOLUTIONS. Get Air Freight Standardized. Get Air Freight Dynamic. Get Air Freight Connected.

CNG burns cleaner than diesel, reducing emissions and greenhouse gas output (Lowe, 2007). Remember, when making the switch, ensure proper infrastructure, such as refueling stations, is available for your chosen fuel type to maintain efficient operations (Freight Transport Association (FTA), 2006a). Khare, M. & Button (eds.),

As a local rail service provider, it’s Conrail’s job to make sure that customers’ freight shipments are safely and efficiently moved between their rail sidings and the long-distance freight trains operated by CSX and Norfolk Southern. In 2007, it expanded its operations from Northern New Jersey to Staten Island, New York.

Still, the requirement is not new and has been under development for a number of years following a milestone vessel collapse in 2007. Ports, which are already at high capacity as a result of the profusion of larger vessels, may face further bottlenecks to ensure that containers have been weighed.

According to IHS Markit, March US purchasing manager’s index (PMI) was the second strongest since data collection began in May 2007. In 2019, it re-acquired HD Supply, a company it sold in 2007. Maersk is one to keep an eye on as it builds its logistics capabilities beyond its ocean freight transportation services.

A behemoth in the logistics industry, UPS has operations in shipping, air freight, trucking, last-mile delivery and drone delivery. FedEx Corporation FedEx , previously known as Federal Express, is an American multinational freight company founded in 1971 as a system for urgent deliveries. Kuehne + Nagel Inc. Jacobs in 2011.

While freight volumes and the supply of trucks and drivers constantly strive for equal balance, they often fall short. Here are the five key freight trends worth watching in late 2019. Freight volumes gain strength. In short, it is a good freight year paired with an exceptional capacity year.

In fact, the company helps its supply chain both measure its carbon impact but also provides solutions, such as right-sizing packages to maximize trailer capacity and thus reduce the number of deliveries. So, we are currently collaborating with our entire supply chain to reduce the overall environmental impact.”.

We organize all of the trending information in your field so you don't have to. Join 102,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content